How to consider a B/BB US high yield strategy within a portfolio

Key points:

- For investors who wish to exclude CCC and below rated assets, but still want to include high yield exposure in their asset allocation, a B/BB approach may offer a compelling solution.

- With an attractive long-term risk/return profile compared to the broad US high yield and investment grade markets, there are different ways that a B/BB strategy can be positioned in a portfolio.

- Today, there is a strong valuation argument for a B/BB strategy, with yields that capture most of the broad US high yield market yield and higher quality bonds priced at a significant discount to par.

The US high yield market has performed well in 2023, offering investors attractive all-in yields and a healthy fundamental backdrop during a year that has been marred with uncertainty and surprises. Many high yield companies came into 2023 having taken advantage of cheap borrowing costs from previous years. They have, therefore, largely been able to weather the rising rates environment without needing to refinance. In many cases they have also used free cash flow to pay down debt and de-lever. This can be seen by the fact that both high yield leverage and coverage ratios are coming off historically strong levels, albeit starting to deteriorate towards the end of 2023 as the ‘higher for longer’ interest rate environment drives dispersion higher. This is particularly seen amongst more levered, capital-intensive companies that do not have the cashflow to absorb significant interest rate increases.

Although this increasing dispersion is leading to a pick-up in default activity, driven particularly by a larger proportion of distressed exchanges and borrowers who also have a loan component in their capital structure which is more immediately impacted from higher rates, we continue to believe that corporate fundamentals remain robust enough to prevent the default rate of the US high yield bond market from increasing to a level significantly higher than its long-term average (3.3% according to JP Morgan).

In this environment, we think that a higher quality high yield strategy offers compelling opportunities to investors who are seeking a yield pick-up from investment grade but remain concerned about the macro environment and want to avoid the part of the high yield market which has historically carried the most default risk. Based on our outlook for the economy and current valuations, we believe that this portion of the US high yield market can deliver attractive total returns over the next 12 months and beyond.

Understanding the high yield credit spectrum

For some investors, accessing the full spectrum of the high yield market is not possible due to capital risk or regulatory requirements. For others, it may be possible, but concerns around default rates may dictate a preference for a higher quality approach. An option for such investors may be to take a more selective approach to high yield and invest via a B/BB strategy rather than avoid high yield altogether.

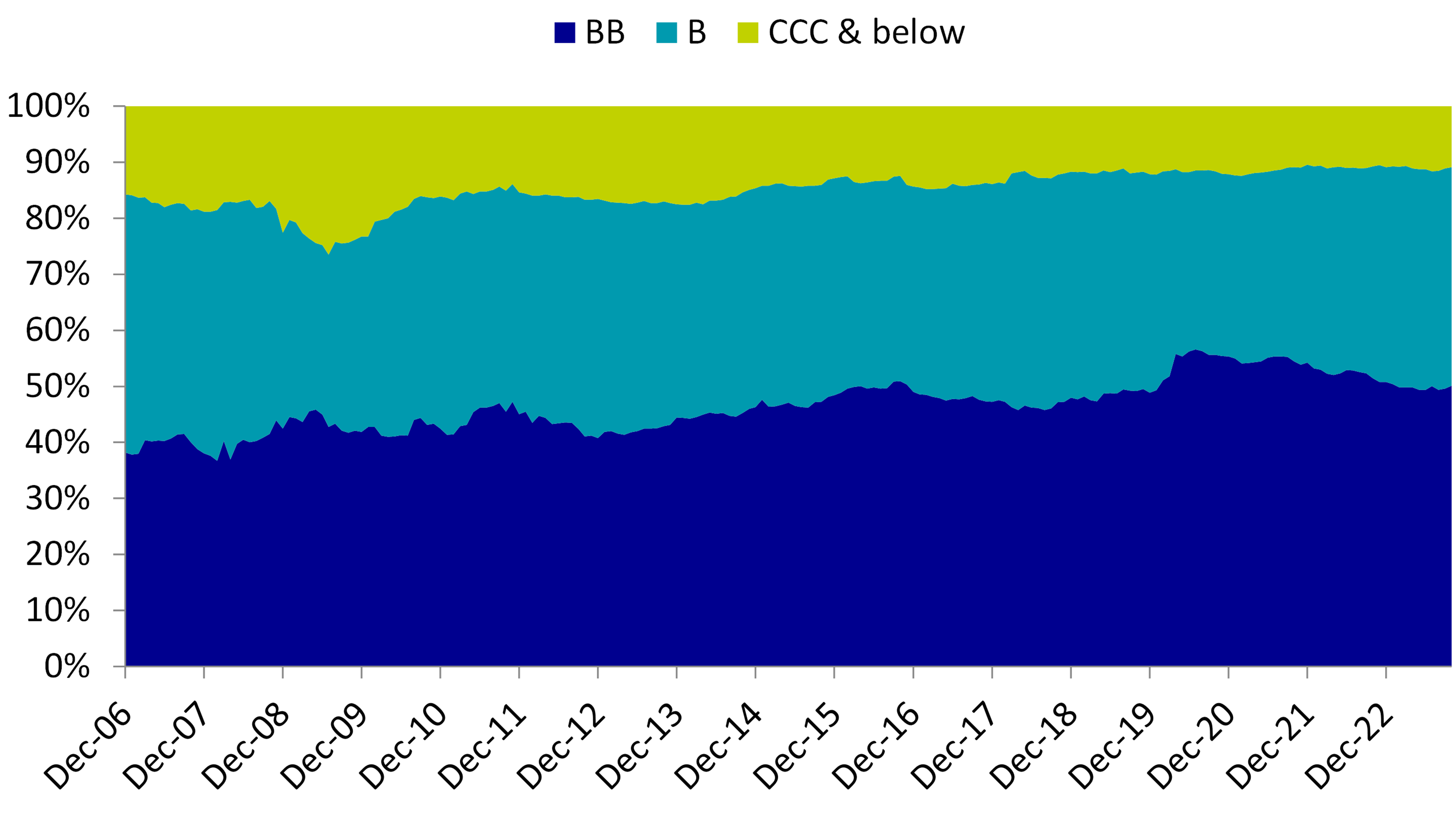

This selective approach to high yield investing does not have to feel like a compromise. Firstly, over the past few years, there have been a wave of upgrades within the US high yield market

Breakdown of the US high yield market by credit rating buckets

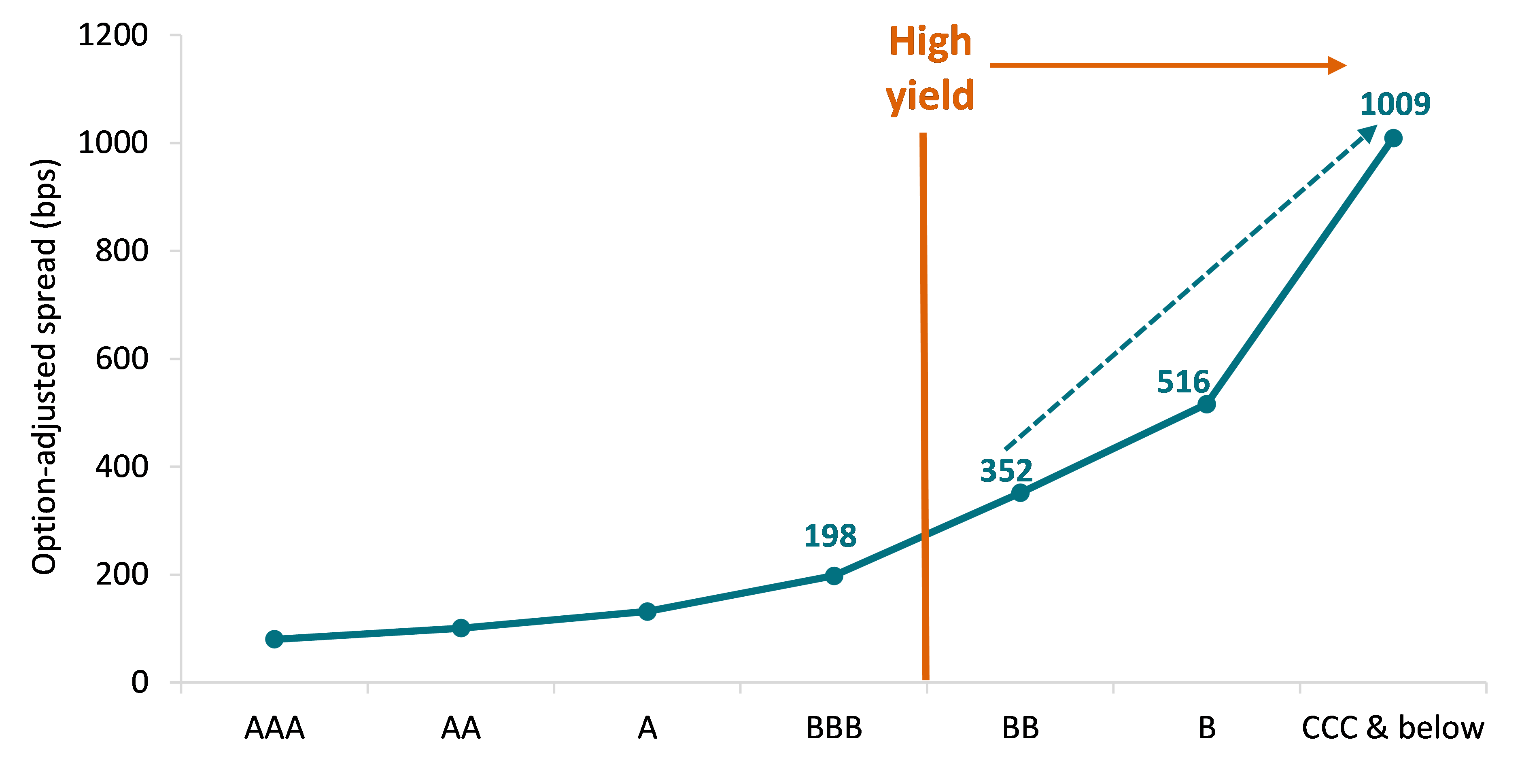

Despite representing the smallest rating bucket by market value, the CCC and below component accounts for the largest proportion of default activity within the US high yield market. We believe that the ‘truest’ way of measuring the credit rating spectrum is on an exponential rather than linear scale, with the credit curve acting as an indicator of underlying default risk, measured in spread (basis point) terms. Credit spreads increase exponentially down the curve to compensate for the underlying credit risk, highlighted by the chart below.

This chart, which plots the average spread of different rating buckets across the full US credit spectrum over a 20-year period, shows that the spread differential between BBB and BB rated securities is 154bps, whereas the difference between B and CCC rated securities is higher at 493bps. Therefore, we may consider that, despite BBB and BB securities being differentiated by rating agencies in terms of ‘investment grade’ versus ‘high yield’, they have more in common than BB securities have with CCC securities.

Plotting the US credit spectrum by average spread*

Source: AXA IM, ICE BofA, as of 31 October 2023. * Average spread relates to a 20-year period covering 31 October 2003 to 31 October 2023.

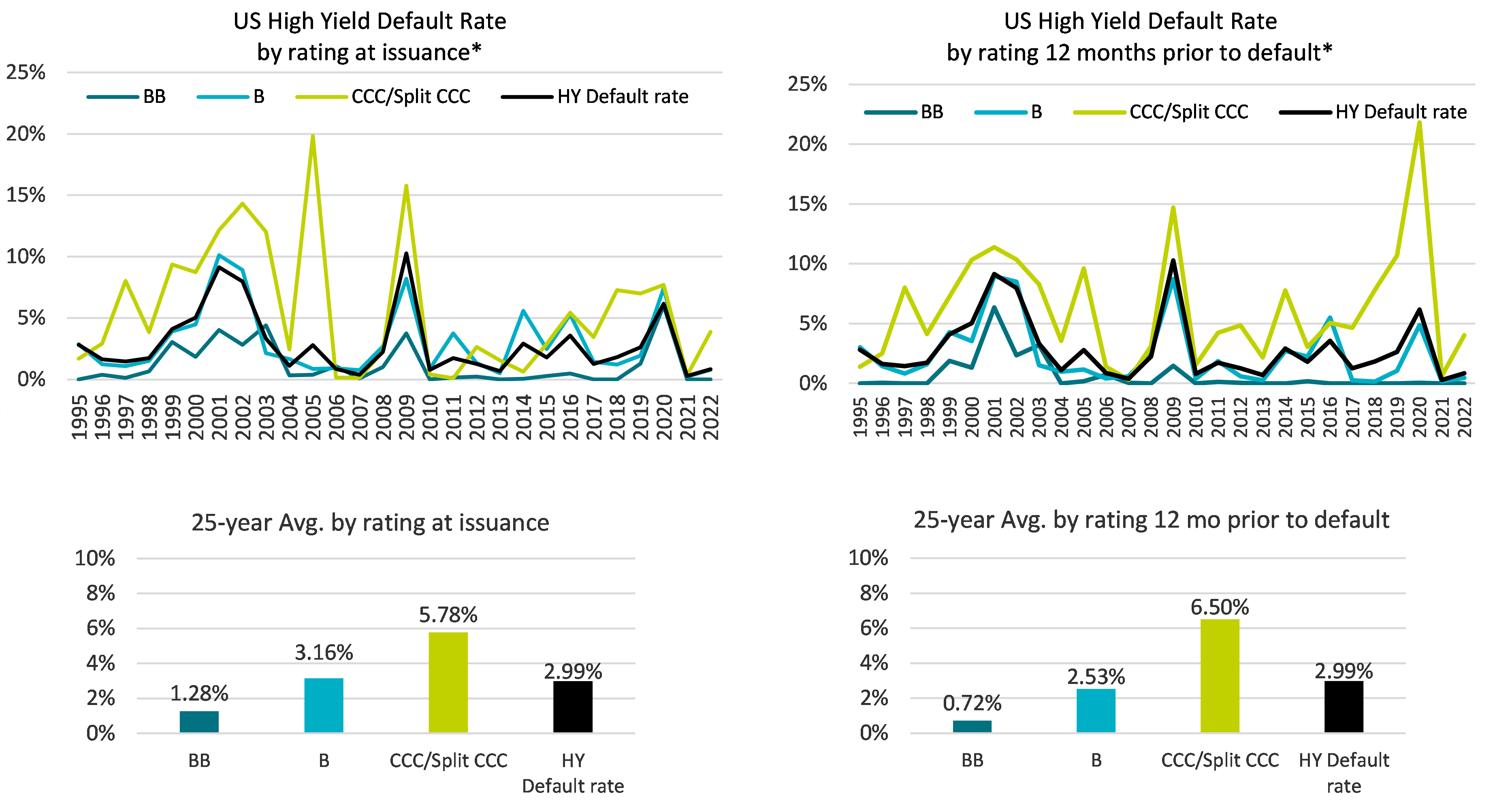

This exponential credit risk is reflected in the fact that the bulk of historical high yield default activity has occurred within the CCC rated bucket. Looking at the 25-year average default rate the largest component of this is CCC/split CCC, tracking at around double the overall high yield default rate of 2.99% for this period:

Source: JP Morgan as of 31 December 2022. *Evolution of default rate taking into account full calendar year data, including distressed exchanges. For illustrative purposes only. Investing involves risk and past performance does not guarantee future results. No assurance can be given that the strategy will be successful or achieve its objectives.

That is not to say that we do not like investing in CCC rated securities. To the contrary, we find plenty of opportunities in improving CCC rated credits that may be penalised by rating agencies for having higher leverage and lower asset values, but which we believe have sound fundamentals and hence less business or operational risk. We feel comfortable holding these credits, however believe that robust, prudent credit analysis and active management are required to ensure that we try to avoid losses and defaults.

Ways to think about positioning a B/BB strategy within a diversified portfolio

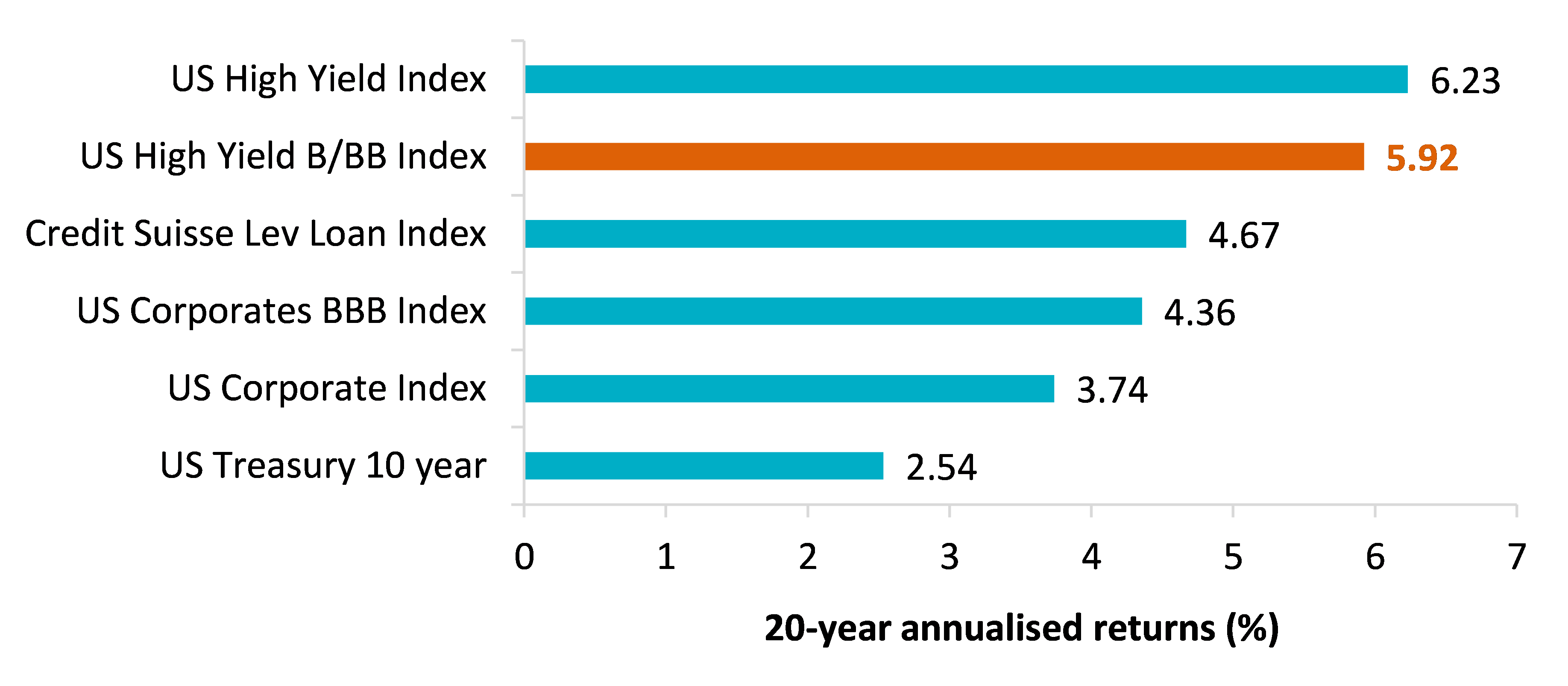

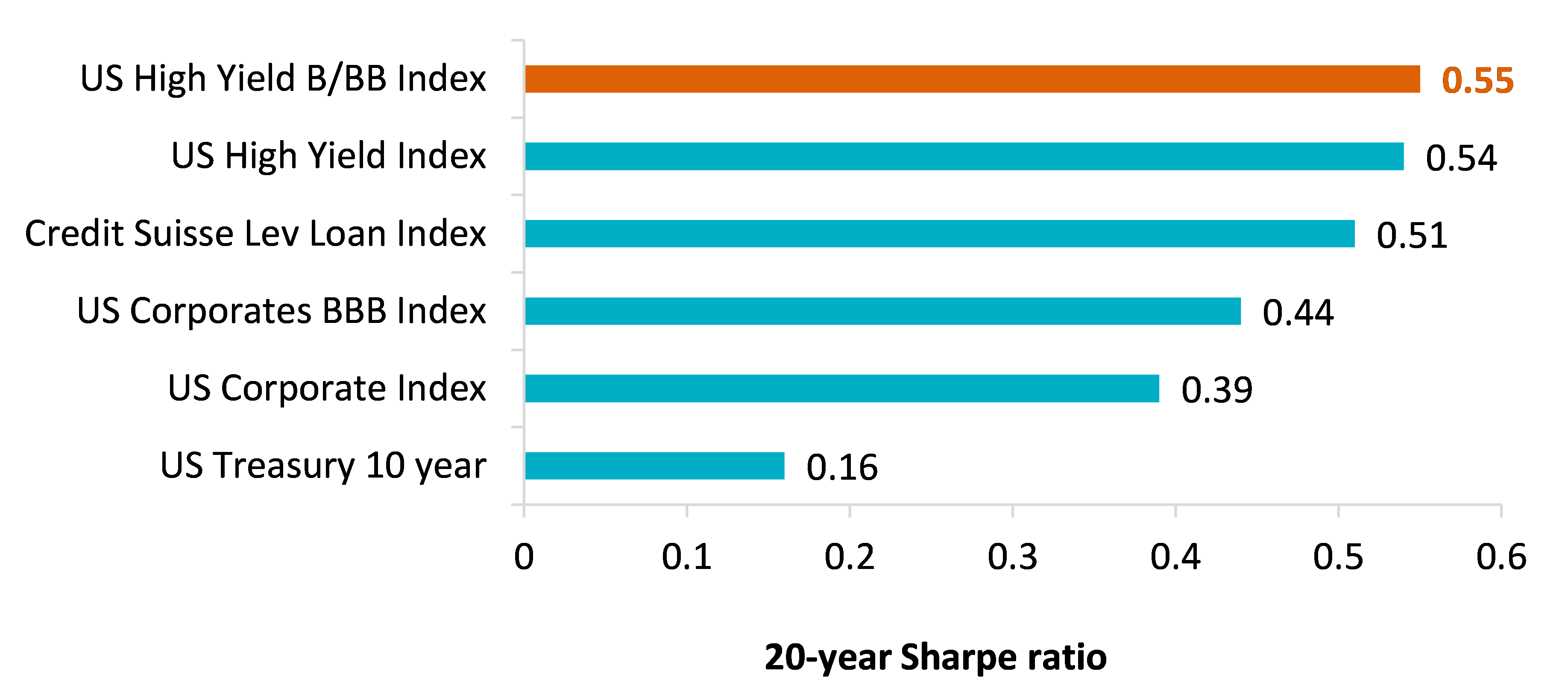

The chart below shows the 20-year annualised returns of the B/BB US high yield universe compared to other US fixed income asset classes. Historically, this universe has captured a large percentage (95%) of the overall US high yield market return, despite carrying significantly lower default risk. It has also outperformed the broad US investment grade market:

Source: AXA IM, ICE BofA, eVestment, as of October 31, 2023.

When considering the volatility of these asset classes, the B/BB US high yield universe is even more compelling on a risk-adjusted return basis, with a higher Sharpe ratio than both the broad US high yield and investment grade markets:

Source: AXA IM, ICE BofA, eVestment, as of October 31, 2023.

Investment grade potential

The charts above suggest that a B/BB strategy can be used as a compliment to an investment grade allocation. While the volatility is higher for the B/BB Index compared to the US Corporate Index, it has provided investors with around 220bps of annualised outperformance for this additional risk, resulting in the improved Sharpe ratio.

By focusing on the B/BB component of the high yield market, investors may also place greater emphasis on larger high yield issuers which offer quasi-investment grade credit quality but with higher yields, as well as potential rising stars to investment grade. Ford is an example of this – a company that was the largest issuer in the US high yield market (~3% or $40 billion of the index market value) which has recently been upgraded by S&P to BBB-

There are also current market trends that we believe could provide a further benefit to higher quality high yield strategies. We are entering a period where company management teams are highly incentivised to de-lever their balance sheets after many years of cheap debt that companies took advantage of. Today, debt is expensive, even relatively speaking for BB or investment grade rated companies. Companies are using asset sales and equity raises to lower the amount of debt in their capital structure. This results in them keeping interest rate expense closer to what they had during a low-rate environment and attracts upgrades from credit rating agencies as it improves their credit quality. In the past, we would not see a lot of opportunities for credit improvement in double-B or single-B rated issues, however that has changed in today’s environment.

Why a B/BB US high yield strategy is attractive today

A B/BB strategy may reduce an investors’ sensitivity to overall default risk in the high yield market if a ‘higher for longer’ rate environment leads to a significantly weaker corporate fundamentals than we are expecting. We believe strategies like B/BB with longer duration are also well positioned right now to benefit from a potential peak in Fed Funds rate and the potential for rate cuts in 2024. As the table below shows, this should not come at the expense of much yield give-up, with the B/BB component capturing over 90% of the overall market’s yield-to-worst.

Source: ICE BofA as of 14 November 2023. Market data provided for the following indices: ICE BofA BB-B US High Yield Constrained Index (HUC4); ICE BofA US High Yield Index (H0A0); ICE BofA US Corporate Index (C0A0).

While some investors may prefer to have access to opportunities across the full spectrum of the US high yield market, a B/BB strategy may be a suitable solution for those who are unable, or would rather avoid, high yield bonds rated CCC and below. A B/BB US high yield strategy has the potential to provide an attractive risk/return profile in relation to the broad US high yield market, as well as offering investors an attractive pick-up from investment grade without adding too much additional credit risk.

Disclaimer

Esto es una comunicación publicitaria. Ha sido preparado con carácter meramente informativo y no constituye una oferta en un folleto en particular o una invitación para cerrar un trato, comprar o vender ningún instrumento financiero o participar en ninguna estrategia de negociación, incluyendo la prestación de servicios de inversión o análisis financiero.

Este documento ha sido preparado por AXA Investment Managers Paris, S.A., Sucursal En España. A pesar de los esfuerzos dedicados a la revisión del contenido de este documento, no se garantiza de manera implícita o explícita que la información aquí contenida sea exacta y completa. Dicha información podrá ser modificada y/o actualizada sin previo aviso. Ni AXA Investment Managers, sus sucursales, filiales y asimiladas, ni ninguna otra compañía o unidad perteneciente al Grupo AXA, y ninguno de sus directores o empleados podrán ser considerados responsables directos o indirectos de la información aquí contenida.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A., Sucursal en España La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión. La información aquí contenida tiene carácter publicitario y se refiere a uno o varios sub-fondos de AXA IM FIXED INCOME INVESTMENT STRATEGIES (la IIC), una institución de inversión colectiva inscrita en la Comisión Nacional del Mercado de Valores (CNMV) con el número 867 (www.cnmv.es), donde puede consultarse la lista actualizada de entidades comercializadoras en España de la Sociedad (los Distribuidores españoles). Tenga en cuenta que la sociedad gestora se reserva el derecho, en cualquier momento, de dejar de comercializar la IIC en España, toda vez que se cumplan los requisitos locales y realizado las notificaciones pertinentes.

La clasificación del Fondo con arreglo al SFDR puede estar sujeta a ajustes y modificaciones, ya que el SFDR ha entrado en vigor recientemente y algunos aspectos del SFDR pueden estar sujetos a interpretaciones nuevas y/o diferentes de las existentes en la fecha del presente documento. Como parte de la evaluación continua y el proceso actual de clasificación de sus productos financieros con arreglo al SFDR, la Sociedad Gestora se reserva el derecho, de acuerdo con la normativa aplicable y la documentación legal del Fondo y dentro de los límites de la misma, a modificar la clasificación del Fondo de vez en cuando para reflejar los cambios en la práctica del mercado, sus propias interpretaciones, las leyes o reglamentos relacionados con el SFDR o los reglamentos delegados actualmente aplicables, las comunicaciones de las autoridades nacionales o europeas o las decisiones judiciales que aclaren las interpretaciones del SFDR. Se recuerda a los inversores que no deben basar sus decisiones de inversión únicamente en la información presentada en el SFDR.

Para más información sobre aspectos de sostenibilidad, consulte el siguiente enlace: Inversión Responsable | AXA IM ES (axa-im.es)

Este documento contiene breve información sobre el sub-fondo y no detalla todos los posibles riesgos u otros aspectos importantes relativos a su potencial inversión. Las decisiones de inversión se realizarán sobre la base de la lectura y entendimiento de la información contenida en el último folleto de la Sociedad, datos fundamentales para el inversor (DFI) y los últimos informes económicos anuales y semestrales. Los Distribuidores españoles facilitarán a cada inversor, con carácter previo a la suscripción de las acciones del Sub-fondo, una copia traducida al español del DFI y el último informe económico. Podrá obtener un resumen en español de los derechos de los inversores en el siguiente enlace Resumen de los derechos del inversor - AXA IM España (axa-im.es) .

En caso de insatisfacción con los productos o servicios, usted tiene derecho a presentar una queja ante el comercializador o directamente ante la sociedad gestora (más información sobre nuestra política de quejas disponible en Nuestras políticas internas y otras informaciones importantes - AXA IM España (axa-im.es) y también consultando https://www.axa-im.es/servicio-de-atencion-de-quejas-y-reclamaciones También tiene derecho a emprender acciones legales o extrajudiciales en cualquier momento si reside en uno de los países de la Unión Europea. La plataforma europea de resolución de litigios online le permite introducir un formulario de reclamación formulario de reclamación y le informa, en función de su jurisdicción, sobre sus vías de recurso .

Asimismo, una copia de la memoria de comercialización, siguiendo el modelo establecido por la CNMV, estará disponible a través de los Distribuidores españoles. La documentación obligatoria oficial estaré disponible a través de los Distribuidores españoles, en versión impresa o digital, y también disponible bajo petición marcando +34 91 406 7200, escribiendo a información@axa-im.com o consultando www.axa-im.es , donde se podrá obtener información sobre los valores liquidativos de las clases de acciones disponibles en España, así como un resumen de los derechos de los inversores.

Se recomienda obtener más información y recibir asesoramiento profesional antes de llevar a cabo una decisión de inversión. Tenga en cuenta que el valor de una inversión puede fluctuar al alza o a la baja y que rendimientos pasados no garantizan rendimientos futuros. Las proyecciones presentadas son una estimación de la rentabilidad futura basada en datos de la variación de esta inversión en el pasado, y en las condiciones actuales del mercado, y no constituyen un indicador exacto. El rendimiento obtenido puede variar en función de cómo evolucione el mercado y de cuánto tiempo se mantenga la inversión o el producto.

AXA Investment Managers Paris, S.A., Sucursal en España, con Código de Identificación Fiscal W0024065E, inscrita en el Registro Mercantil de Madrid, Tomo 41006, Libro 0, Folio 1, Sección 8, Hoja M-727252, con domicilio Paseo de la Castellana 93, 6ª planta e inscrita en la Comisión Nacional del Mercado de Valores con número de registro oficial 38 como una Sociedad gestora del espacio económico europeo con sucursal en España.

AXA IM y BNP Paribas AM están fusionándose y reorganizando progresivamente nuestras entidades legales para crear una estructura unificada.

AXA Investment Managers se unió al Grupo BNP Paribas en julio de 2025. Tras la fusión de AXA Investment Managers Paris con BNP PARIBAS ASSET MANAGEMENT Europe y sus respectivas sociedades holding el 31 de diciembre de 2025, la nueva compañía ahora opera bajo la marca BNP PARIBAS ASSET MANAGEMENT Europe.