Bonds, I presume?

Bond bearishness continues, but the market is not doing much beyond reacting to supply and demand, alongside the usual flow of economic data, and expectations about central banks. My view is we are in a different regime to the interest rate-resetting years of 2022-2024. It’s more of a bond-normal regime. Curve steepening is cyclical and will probably extend further with more rate cuts. Yes, there are concerns about inflation and fiscal balances, but that might all be priced in. The big bond losses are potentially behind us and today the fixed income markets are doing what they are supposed to – provide income with a total return volatility that is typically a third that of equities.

- I still like short duration credit, inflation-linked bonds, high yield, and increasingly gilts

- I’m worried about US equities, interference with the Federal Reserve, and the noise around gilts

Rates regime reset

Long-term government yields have continued to rise and yield curves continue to steepen. The trend started in early 2022 with the pivot towards tighter monetary policy in response to the post-pandemic inflation shock. However, the trend has extended beyond the tightening cycle, with yields rising even as central banks have been cutting rates. Monetary policy expectations drive the short end of yield curves. The decline in global inflation rates since 2022 has allowed central banks to ease, a process that the market expects to continue, at least in the US and in the UK (Europe has already done a lot). What drives the long end are expectations on growth and inflation, and premiums related to fiscal policy, as well as other risks, such as not meeting an inflation target. In the US and UK, inflation has not fallen back enough and fiscal concerns have come more into focus. Hence, curve steepening and some over-dramatic commentary on the future of borrowing costs, public debts and bond pricing.

Dramatically ordinary

In the UK, 92% of the increase in the 10-year government bond (gilt) yield between early 2022 and today happened during the period when the Bank of England took the policy rate from 0.1% to 5.25%. For the 30-year maturity, 79% of the increase in yields between early 2022 and now happened during that policy tightening period. It has been a very similar story in other markets. In 2025, the 10-year gilt has traded within a 46 basis points (bp) range, with the 30-year in a 67bp range. For the US market the ranges have been 80bp and 68bp respectively, and in Germany, 53bp and 81bp. For the whole of 2024, the 30-year yield trading ranges were 104bp, 89bp and 55bp for the UK, US and German markets respectively.

Risk premium steepening

Globally, long yields have risen relative to short rates even with central banks easing. But in terms of volatility, there is nothing unusual about the range of trading in bond markets in 2025 (in September 2022 alone, the range for the 30-year gilt yield was 180bp). But the UK has underperformed. With several changes of prime minister in recent years and, since July 2024, a new government, the market is not convinced that UK policies can deliver a more stable outlook for public finances. If the UK government were to borrow by issuing 30-year bonds today, it would pay 72bp more than if the US government did the same. Good job it isn’t then. Indeed, it does not need to. This week the Debt Management Office cancelled a scheduled auction for 30-year bonds. But it did borrow by issuing 10-year gilts, raising £14bn at a yield of around 4.86% (the order book reached £140bn, showing that higher yields do attract demand from investors). There was no evidence of investors panicking or avoiding buying UK government paper.

Eyes on Reeves

The UK government announced its next fiscal event, the 2025 Budget, will be presented on 26 November. That is later than expected and shows the government needs more time to decide what to do with taxes. Until there is more clarity, gilts could continue to underperform other bond markets. However, a Federal Reserve (Fed) rate cut, or weaker US employment data would allow gilt yields to fall as part of a global response. At any rate, 30-year yields at 5.8% are attractive in my view and the government has shown it has no need to lock into that maturity at these borrowing costs. Outstanding gilts with over 15 years’ maturity now make up just 29% of the total conventional gilt market; that was nearly 50% in 2020. The other bit of potentially good news is that UK growth data has been a bit stronger of late. If there is any change in the Office for Budget Responsibility’s forecasts, there could be some easing of pressure on the fiscal outlook – on a rolling 12-month basis, government cash receipts (taxes) have been increasing by over 7% year on year.

Regime of normal

Global bond yields are not far off what a simple model based on a moving average of nominal GDP growth would suggest. The US is at fair value, as is France; Germany is expensive, and the UK is on the cheap side. It is easy to forget that for a long time, bond yields were kept low by financial repression, and it is only in the last two years they have reverted to more neutral levels. Moreover, yield curve steepening is perfectly understandable. The unusual thing in recent years was the inversion of yield curves – as recently as June 2023, the US 10-year Treasury yield was 100bp lower than the two-year yield. A positive curve gap of between zero and 250bp has been the norm for the best part of the last four decades, and fixed income 101 suggests it is ‘normal’ for curves to slope positively as investors should receive more yield for giving up money for longer. There is more steepening to come in the months ahead – especially if the August US employment report prompts the Fed into cutting by 50bp.

Growth and income in 2025

This year, across fixed income markets, most total returns have come from income. High yield and emerging market debt have been the best sectors for income generation. Long-duration government bonds have best been avoided because, despite some income, price action has been negative. The over 15-year US Treasury index, for example, has a 2.64% income return to date and a 0.68% decline in price return. For long gilts it has been much worse – 2.6% from income but -7.3% from price. The sweet spot has been in short-duration credit strategies or in floating rate asset-backed securities. Growth has come from US equities; European markets have also delivered some growth and decent dividend income. For the balance of the year, short-duration credit and European equity exposure should potentially continue to perform in a similar way.

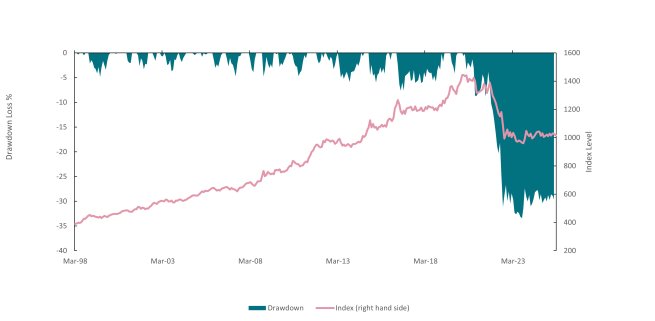

Horses bolted

The final word is about bond bearishness. Concerns about global fiscal trends are legitimate. But there seems to be a misunderstanding about where we are in bond markets. The 2022-2024 period was a rate reset regime. That is when the money was lost. Since then, we are in a bond-normal regime where a lot of time is spent trying to observe the unobservable (term premium, neutral rates, etc.) rather than accepting the cyclical dynamics. The chart below is the drawdown chart for the UK Gilt index. Passive investors in gilts lost more than 30% from the peak and those losses have not been eroded. But the point is that the bulk of this happened in 2022. To lose another 30%, the market yield would need to go to 9%. And I certainly would bet against that happening.

Performance data/data sources: LSEG Workspace DataStream, ICE Data Services, Bloomberg, AXA IM, as of 3 September 2025, unless otherwise stated). Past performance should not be seen as a guide to future returns.

Disclaimer

La información aquí contenida está dirigida exclusivamente a inversores/clientes profesionales, tal como se establece en las definiciones de los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65/UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

© AXA Investment Managers Paris, S.A. 2025. Todos los derechos reservados.

AXA IM y BNP Paribas AM están fusionándose y reorganizando progresivamente nuestras entidades legales para crear una estructura unificada.

AXA Investment Managers se unió al Grupo BNP Paribas en julio de 2025. Tras la fusión de AXA Investment Managers Paris con BNP PARIBAS ASSET MANAGEMENT Europe y sus respectivas sociedades holding el 31 de diciembre de 2025, la nueva compañía ahora opera bajo la marca BNP PARIBAS ASSET MANAGEMENT Europe.