EM reaction: a surprise 500bp rate hike in Turkey in March, month of local elections

- 21 Marzo 2024 (5 min de lectura)

A bold rate hike in March and renewed commitment to tame inflationary pressures

The Central Bank of Turkey (TCMB) hiked their policy interest rate by another 500bp at its March monetary policy meeting, which were at odds with Bloomberg’s consensus expectations of the Bank staying on hold.

The more recent slippage of inflation expectations has indeed further pressured the lira, opening the door for more action from the central bank. Its decision to tighten its macroprudential framework yet again by reducing loan growth limits, three weeks ahead of today’s meeting (on March 1st) had raised doubts about possible political constrains around the central bank upon its ability to deliver further rate hikes, particularly in the context of local elections taking place at the end of the month. This was proven wrong by today’s bold move, the first hike under the new Governor Mr. Fatih Kharan who took over in January after Ms. Erkan’s resignation. Furthermore, the official statement continued to retain a hawkish forward guidance: “Tight monetary stance will be maintained until a significant and sustained decline in the underlying trend of monthly inflation is observed, and inflation expectations converge to the projected forecast range. Monetary policy stance will be tightened in case a significant and persistent deterioration in inflation is foreseen.”

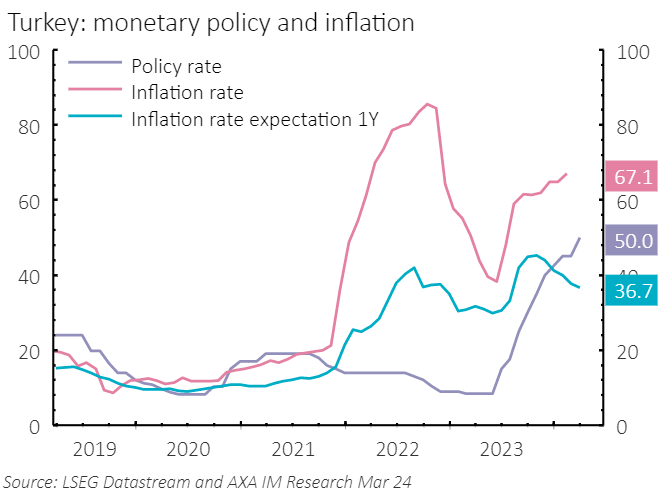

Interest rates have been hiked by a cumulative 4,150bp from 8.5% in May 2023 to 50% in March 2024, as the economic team following the re-election of incumbent President Recep Tayyip Erdoğan was given the mandate to tackle the various imbalances accumulated by the Turkish economy these past years. The most pressing ones included an overheated credit-fueled economy; excessively high inflation and de-anchoring of inflation expectations; massive external financing needs; insufficient reserves at the central bank; significant slippage of public finances and accumulating contingent liabilities. Ten months since the last general elections (May 2023) and just a few days away from local elections (31 March), many of these issues remain, some have worsened. 2023 GDP growth recorded at a staggering 4.5% (4% year-on-year in Q4), but more importantly, the third year of a double-digit contribution from domestic demand, signaling obvious overheating. Monetary policy has become more orthodox, and today’s bold move further improved the credibility of the central bank. Currently, we project inflation to accelerate to above 70% by mid-year and decelerate towards 45% by year-end. At 50%, ex-ante real policy rates compensate for the continuous de-anchoring of inflation expectations and could be a sufficient tight stance to see disinflation taking place in H2 upon a tighter fiscal policy, but we acknowledge that there is a risk of seeing further monetary tightening if inflation pressures fail to decompress as fast as projected.

The inflation outlook remains bleak at the start of 2024, but we still expect disinflation to take place in H2 2024.

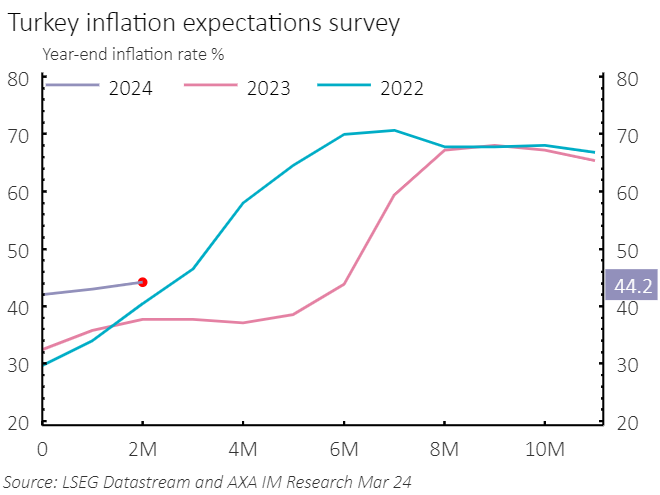

Inflation rate reached 67.1% year-over-year in February 2024 (72.9% for core inflation), more than double since June 2023 when it reached 32.8%. Services prices, in particular, which usually display more stickiness, have posted strong increases, annual inflation in the services sector accelerated further to 94.4%. On the goods side, the recent acceleration in FX depreciation points to deterioration in goods inflation which printed 57% year-over-year in February. Meanwhile, inflation expectations drifted further away from CBRT’s year-end forecast of 36%, with March survey pointing to year-end inflation rate projected at 44.2% up from 40% back in January. Projecting inflation ahead remains a very difficult task; as a theoretical exercise, if we were to apply as of March 2024 the average monthly inflation increases of the past four years, inflation rate would end the year at 49%. We assume a slightly slower pace of inflation as of mid-year on the back of a tighter policy mix (particularly the fiscal stance post-elections) that would dampen domestic demand into H2 2024, bringing the year-end inflation closer to 45% year-over-year.

Local elections (31 March) a few days away...

After having won Presidential and legislative elections back in May 2023, President Erdoğan’s AKP party is hoping to reclaim several major cities’ mayor positions, most importantly Istanbul, lost in 2019, Turkey's commercial hub of 16 million people (20% of the population). Undoubtedly, the AKP has a strong position into these polls. There is an obvious preference for dollar denominated assets ahead of elections in Turkey, and it needs to be seen whether this recent hike and the outcome itself of the ballot will achieve to balance the preference towards lira denominated assets in the next weeks/months. To this respect, President Erdoğan’s recent comments acknowledging that these local elections will be his “final” election seek to alleviate worries that he may call for yet another referendum in order to change the Constitution and grant him more time at the helm of the country. Rendez-vous on March 31st …

Artículos relacionados

View all articles

Webinar: El Ciclo Macroeconómico - ¿Dónde nos encontramos?

- por

- 16 Noviembre 2023 (15 min de lectura)

Climate change: The economic cost of inaction

- por

- 26 Octubre 2021 (5 min de lectura)

UK reaction: Unemployment rises but the focus remains firmly on pay growth

- por

- 16 Abril 2024 (3 min de lectura)

China reaction: momentum accelerated boosted by investment

- por

- 16 Abril 2024 (3 min de lectura)

Disclaimer

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65 / UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

La información aquí contenida está dirigida únicamente a clientes profesionales tal como se establece en los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.