How investors can get on board with sustainable travel and transport

Key points:

- International travel is returning to near pre-pandemic levels, highlighting the sustainability challenges for the sector

- Policymakers are taking decisive action to reduce emissions from transport while new technologies are popularising alternative methods of travel, and helping decarbonise existing ones

- The combination of new policies and technological innovation is creating a wave of long-term investment opportunities

International tourism is expected to return to almost pre-pandemic levels this year,

The answer, quite clearly, is decarbonising methods of transport and travel – but while the answer is simple, the process of getting there is not. However, this journey towards lower carbon travel is underway, and creating potential new opportunities for investors now and in the future.

From electric vehicles and sustainable aviation fuels to micro-scooters, we have seen a wave of innovation in the transportation sector over recent years, with new technologies popularising alternative methods of travel, and helping decarbonise existing ones.

Governments and policymakers are also taking drastic action in a bid to reduce emissions – France has banned short-haul flights where train alternatives exist,

But governments don’t want to put the brakes on international travel and tourism – a sector that contributed 7.6% to global GDP last year and created 22 million new jobs.

For many countries, attracting hordes of foreign tourists is vital to their economy.

However, travel and tourism accounts for between 8% and 11% of total global carbon emissions, according to varying estimates – which is almost certain to increase as travel activity is predicted to surge by 85% from 2016 to 2030.

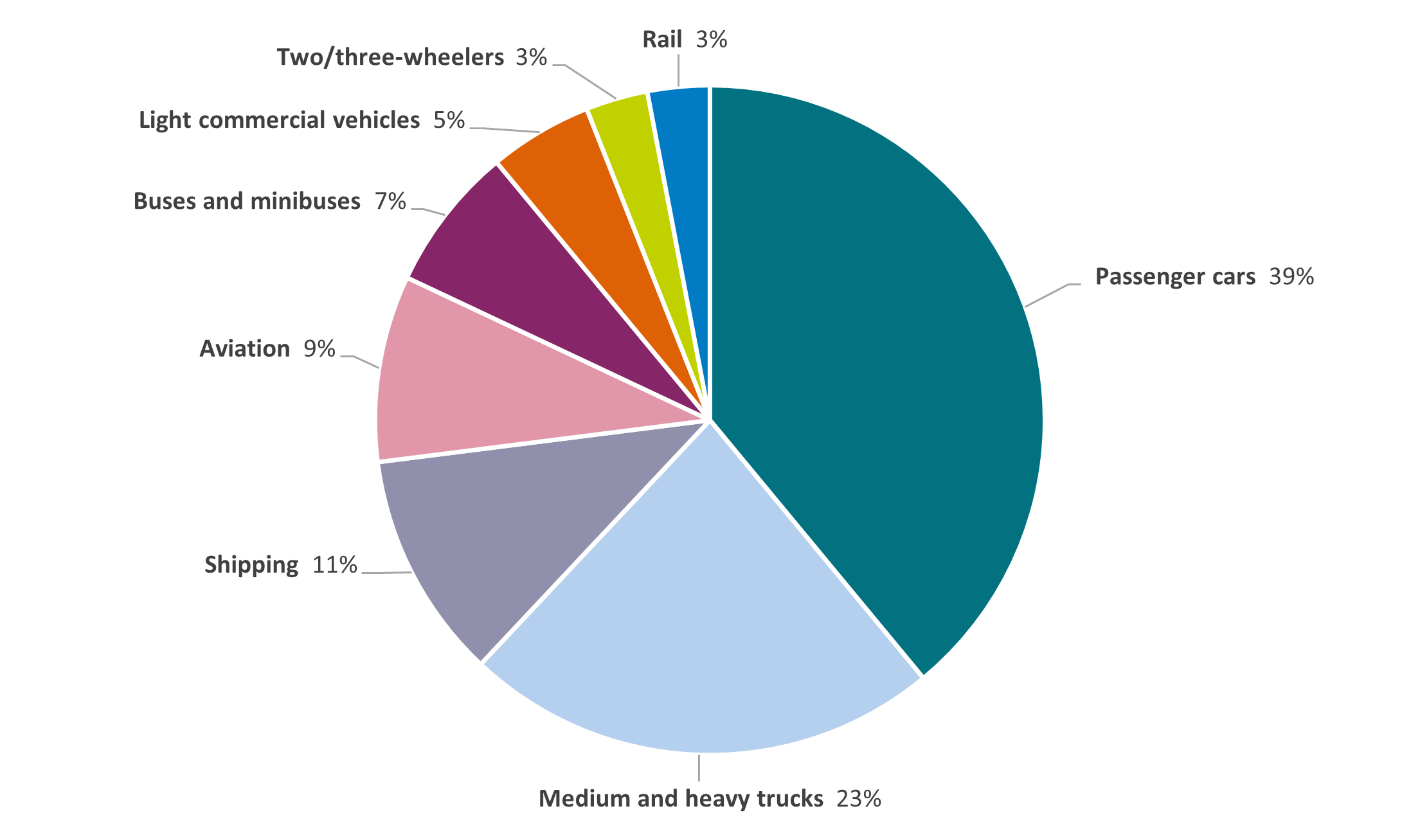

Carbon emissions from transport by sub-sector

Source: Statista, based on 2021 data

Low-carbon fuels

Mile for mile, flying is the most carbon-intensive method of travel – the aviation industry is thought to be responsible for around 5% of global warming.

Many airlines have already made commitments to using sustainable aviation fuel (SAF). A biofuel with similar chemical properties to conventional aviation fuel, SAFs have potentially sharply lower greenhouse gas emissions – but are currently expensive and hard to come by.

This may change in future as the US Inflation Reduction Act includes subsidies for SAF production while the European Union is reported to be considering setting SAF usage targets from 2030 for any airline seeking to receive a green label.

Changing consumer preferences can also help shift the dial – a recent survey found that 40% of travellers were willing to pay at least 2% more for carbon-neutral flights.

Meanwhile the cruise industry is the fastest growing tourism sector and is expected to exceed pre-pandemic levels in passenger numbers and revenues by 2026.

Electric vehicles on the rise

Cars are the biggest contributor overall to transport sector emissions, at some 39%, in part due to the sheer number of vehicles on the road.

Sales of electric vehicles (EVs) are expected to rise 35% this year,

Reducing the number of cars on the roads is also another step towards lower carbon emissions. Ridesharing potentially reduces the need for car ownership, particularly in cities, and opens up a new swathe of companies for investors to consider - but a recent study suggests it is pricing that makes the difference between whether ride sharing reduces or increases emissions.

Rail travel has one of the smallest carbon footprints of transport methods,

And while artificial intelligence has had mixed press recently, there’s no doubt it can be helpful in certain areas – in transport for instance, companies are using artificial intelligence and cloud computing to deliver smarter timetables to meet changing customer demand.

Meanwhile electric trains and trams harnessing new technologies including automation can provide low carbon alternatives in cities and new urban developments. The global connected rail market is already estimated to be worth over $92bn and to reach over $143bn by 2030.

At the smaller end of the scale, we are seeing a surge in popularity of micro-mobility – electric bikes and scooters. The COVID-19 pandemic caused a spike in demand for these kinds of powered two-wheelers as an alternative to public transport.

Micro-mobility now accounts for an estimated 16% of trips globally, according to McKinsey & Company. It estimates that the market is worth around $180bn today, with the potential to more than double by 2030 to around $440bn.

Driving potential investment opportunities

The economic downturn and high inflation are likely to mean consumers are more demanding when it comes to spending their money on leisure travel – and they are increasingly aware of the environmental impact and becoming more selective about sustainability issues when travelling.

There is ongoing impetus from governments and policymakers, which we expect to only increase as they strive to meet climate targets, both in encouraging lower carbon forms of travel and granting incentives for investment in decarbonisation.

Companies everywhere are setting sustainability targets, many including emissions from business travel, which represents nearly a third of all travel spend.

As the market continues to return to, and likely exceed, pre-pandemic levels, we see scope for potential investment opportunities for those who want to play a part in the journey to sustainable travel while also seeking financial returns.

Disclaimer

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65 / UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento/ material audiovisual. La información incluida en este documento/ material audiovisual se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

La información aquí contenida está dirigida únicamente a clientes profesionales tal como se establece en los artículos 205 y 207 del texto refundido de la Ley del Mercado de Valores que se aprueba por el Real Decreto Legislativo 4/2015, de 23 de octubre.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).»

© AXA Investment Managers Paris, S.A. 2023. Todos los derechos reservados.

AXA IM y BNP Paribas AM están fusionándose y reorganizando progresivamente nuestras entidades legales para crear una estructura unificada.

AXA Investment Managers se unió al Grupo BNP Paribas en julio de 2025. Tras la fusión de AXA Investment Managers Paris con BNP PARIBAS ASSET MANAGEMENT Europe y sus respectivas sociedades holding el 31 de diciembre de 2025, la nueva compañía ahora opera bajo la marca BNP PARIBAS ASSET MANAGEMENT Europe.