Inflation Review: The "greedy beast" of inflation is still breathing, in particular in services

- 02 Febrero 2024 (5 min de lectura)

Key points:

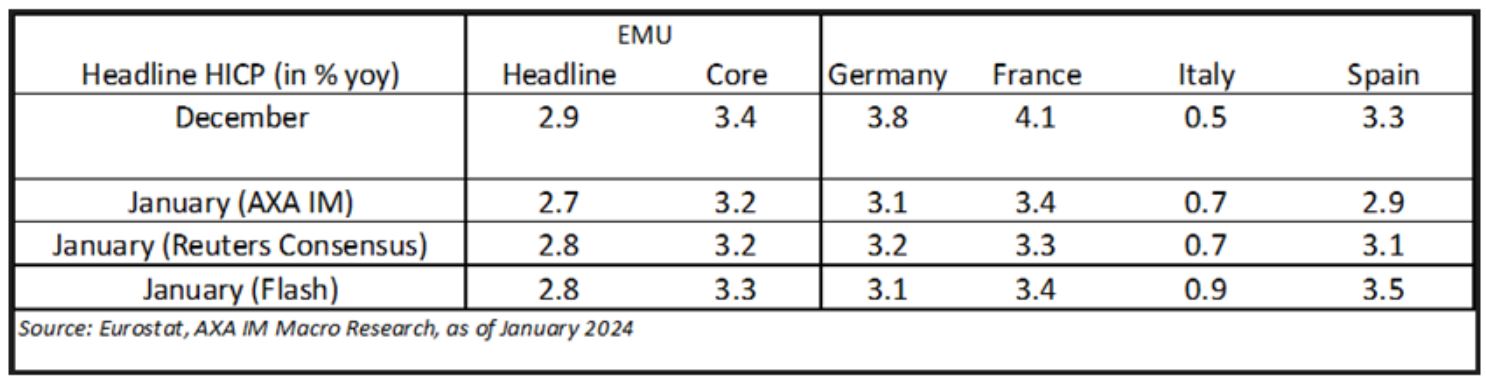

- Both euro area headline and core inflation dropped by 0.1 point, respectively to 2.8% y/y and 3.3%, slightly above consensus expectations

- At face value, these are good news. But services inflation is stickier, being flat at 4% for the third successive month.

- We believe it will only reinforce ECB's dependence towards data, in particular on services prices and wage data, while keeping an eye on other components subjected to upside risks from tensions in the Middle East.

Euro area headline inflation decelerated to 2.8% y/y in January (-0.1 percentage point from December), slightly above our forecast (2.7%) but in line with consensus.

Core inflation dropped to 3.3% y/y, 0.1 pp below December level, but slightly above our forecast and consensus (3.2%). Crucially, the decline was only driven by non-energy industrial goods (NEIG) (2.0% y/y; -0.5pp from December), while services prices were flat at 4.0% for the 3rd successive month. Energy prices were a bit stronger than our forecast, declining by only -6.3% y/y (+0.9% on a monthly basis). Food alcohol and tobacco (FAT) came at 5.7% y/y, in line with our forecasts. Processed and unprocessed food continued to decelerate, respectively at 5.7% and 5.3%.

Services prices are flat at 4% (again), likely to maintain the ECB on the cautious side

Putting us in the ECB's shoes, this January print doesn't change much. At face value, both headline and core inflation decelerated, despite several measures of support, deployed during the energy crisis, being removed. The ECB probably pencilled in a stronger inflation in January as they were forecasting 2.9% on average for Q1 2024 while January is our highest monthly print. The big picture is (ever so slightly) improving but services momentum isn't.

The ECB cares much more about services inflation which now accounts for 44.5% of total inflation basket. The latter came at 4.0% y/y, at the same level for three successive months. Looking at the monthly pace (-0.1%), it is the same than January 2023 and 2022, largely above average of 2015-2020 (-0.6% m/m). It is partially explained by some increasing taxes such as in VAT for German restaurants or package holidays methodological changes, but the difference is noteworthy. That means companies continue to hike prices at a significant pace. The reasons behind such pricing behaviour are probably to be matched with past inflation, wages anticipations and resilient corporate profit margins.

Wage growth is also key for the ECB. Some figures surrounding ongoing wage negotiations seem high, in particular in Germany or in the Netherlands (negotiated wages just came out at 6.9% y/y, flat from December). After 4.4% in Q2 2023 and 4.7% in Q3, we forecast EMU negotiated wages to reach 4.4% in Q4. We can't exclude something a bit higher, in particular after the surge of hourly wages in Italy in December (7.9% y/y in Q4, from 2.7%). A large part of it is an artefact as it reflects an advance payment, but it will mechanically boost the aggregated index.

Last but not least, we fear components which are currently driving down inflation, may face upside risks as tensions in the Red sea and in the Middle East have not faded and its impact on good and possibly food prices are yet to be seen. Some studies are pointing to an impact worth of 0.1-0.2 pp on core inflation from doubling shipping cost.

There is more to learn from the final January release

Preliminary data give … preliminary conclusions but everything else equal, weight changes are likely to boost inflation figures in 2024. Indeed, services weight rose to 44.5% (+1.3 p) while the other majors components declined (NEIG to 25.70% (-0.57 p), FAT to 19.47% (-0.51p) and energy (9.94% (-0.29 p). Nowadays, services inflation is the stickier component, so rising weight push inflation on the upside. Lower weights from components with downward price pressures also lower their contribution. It is likely to boost average inflation by some bps in 2024. We will have full details for items and countries by February 22.

Another interesting details will be to look at industries usually keen to increase their prices during January. It is around 15% of the basket (excluding energy, fresh food), twice the usual monthly rate and mostly concentrated on services like insurance products, subscriptions…etc (source: "New facts on consumer price rigidity in the euro area", E.Gautier & al. Sep 2023). Their pricing behaviour consider what happened last year but also what they expect for this year and in particular labour cost.

January inflation figures have been only slightly stronger so there are no reasons to adjust our forecasts yet, in particular as we need to see final weights for countries and items. The only change we've made is removing the normalisation of monthly train ticket in Germany. In fact, we were pencilling in a large increase this year, but the government recently extended the measure into 2024. The latter had a significant impact on our forecasts. We lower accordingly our euro area core inflation by approximately 0.15pt on average for 2024 and 0.1pt for headline. We now project both headline and core at 2.5% for 2024 and 2.1% for 2025 (also for both headline and core).

Disclaimer

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65 / UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

La información aquí contenida está dirigida únicamente a clientes profesionales tal como se establece en los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.