US reaction: FOMC still sees three cuts as inflation outlook not really changed

- 21 Marzo 2024 (3 min de lectura)

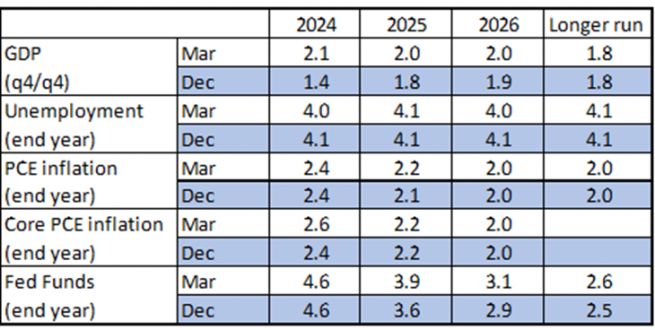

The Federal Reserve left policy rates unchanged at its March meeting, the Fed Funds target range at 5.25-5.50% and interest on reserve balances at 5.40%. The Fed continued with its current pace of QT. These decisions were by unanimous decision, as broadly expected. The Fed’s short-term outlook as described by its accompanying statement was barely changed. The statement removed the description that jobs growth had “moderated since early last year”, simply stating that “gains have remained strong”. There was more adjustment to the Summary Economic Projections (SEP) (see Exhibit 1 below). Growth expectations were raised for this year (end-year forecast raised to 2.1% from 1.4% in December), in part reflecting an expectation of ongoing momentum from the fast close to last year and stronger labour supply. However, future years growth was also edged higher to stay at 2.0% in subsequent years – ahead of the Fed’s assessment of trend growth. However, the Fed’s unemployment forecast was barely adjusted, bouncing around the Fed’s view of the long run rate. Core PCE inflation forecasts were also raised for this year to 2.6% from 2.4% in December, but forecasts continued to show headline (and core) inflation returning to the 2.0% target in 2026, with headline inflation edging higher to 2.2% (from 2.1%) next year.

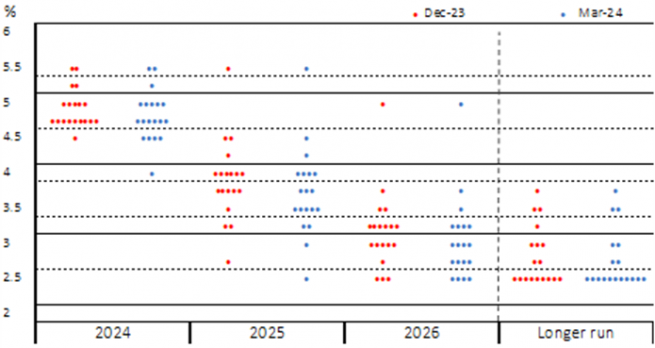

Most importantly, the median rate outlook of the Committee continued to see three rate cuts for 2024. Exhibit 2 illustrates that in turn the median stability disguised a modest adjustment in the distribution of the Committee’s views: more participants considered policy with fewer than three cuts this year and fewer saw more, but the majority of the Committee continued to expect three or more cuts over the year. However, expectations for cuts in 2025 were reduced to 75bps (from 100bps) and 2026 still saw 75bps, but now to 3.25-3.00% from 3.00-2.75% in December. The median rate outlook for the long-term rate also increased to 2.6% from 2.5%, with the central tendency widening to 2.5-3.1% (from 2.5-3.0%). All suggests that the Fed’s confidence in the longer-term easing it will need to deliver has reduced, even if its short-term outlook has been less effected.

Fed Chair Powell’s press conference broadly addressed the current market zeitgeist: that higher inflation at the start of the year would derail the Fed’s expectations of rate cuts for this year. Powell was measured and consistent saying that the Fed needed more data to have sufficient confidence to ease policy. He said that January and February’s data had not added to that confidence, but nor did he think it had changed the picture. He repeated that the Fed would “approach the question carefully”. The Fed Chair reiterated that inflation had made “substantial progress”, but more was needed. He concluded that the ‘dots’ showed that most members expected to have sufficient confidence to “begin to dial back the level of restrictiveness .. at some point this year”. Separately, the Fed Chair went someway to explaining the change to the Fed’s SEP outlook of firmer growth but no meaningful change to unemployment by highlighting stronger labour supply.

Our own view is for now unchanged. We continue to expect to see some moderation in services inflation over the coming months to provide sufficient confidence for the Fed to begin cutting in June, but acknowledge that that case has yet to be made by the data. We continue to forecast four cuts for this year – rather more than the Fed and markets now consider. This view sees the Fed quickening the pace of cuts by year-end. Our own view is that the economy is likely to be a little softer than the Fed’s current outlook and we think the Fed will accelerate cuts as softness becomes apparent. However, we acknowledge that this cut is in the balance and a firmer growth outlook could see us shift this view. We still expect the Fed Funds Rate to close 2025 at 3.75-3.50%, now below the FOMC’s projections. We also do not think that the timing of Fed cuts will be impacted by this year’s Presidential election, with no evidence that it has been impacted by elections over the past four decades.

The Fed Chair also revealed that the Fed had started to discuss tapering the pace of QT at this meeting. He explained that the Fed believes that by reducing the balance sheet more slowly it will allow a more even distribution of reserves between banks and could avoid liquidity issues, in turn potentially allowing the Fed to ultimately reduce reserves further. This is the argument Dallas Fed President Logan advanced at the start of the year. Powell said that the Fed would make a decision on the slower pace “fairly soon”. Since Logan’s comments at the start of the year we have expected the Fed to announce a slowing of the pace (broadly to halve the pace) in June, effective in July. We maintain this view, but acknowledge the risks of an announcement at the next meeting.

Market reaction was mixed. Short-end rates pared back fears that short-term inflation prints had derailed Fed rate cut expectations. The probability of a June cut rose to 84% from 68bp before the release and December’s pricing gained 9bps, to see the probability shift from three cuts by year-end not being fully priced to now seeing a chance of more than 25% of four cuts. 2-year UST yields dropped 7bps to 4.61% and the dollar fell by 0.5% against a basket of currencies. Stocks also received the news well, particularly the outlook for stronger growth, but still an easing in short-term policy and the S&P 500 equity index gained 0.9% on the release setting a new record high in excess of 5200. However, 10-year UST yields were more concerned about fewer rate cuts further out and the prospect of the Fed mulling a higher LR FFR. 10-year yields initially fell to 4.23% from 4.28%, but then revered to rise to 4.32% before settling at 4.27% at the time of writing, just 1bp lower.

Related Articles

Ver todos los artículos

ECB Review: No commitment, no guidelines, no…thing

- por François Cabau,

- 19 Julio 2024 (3 min de lectura)

UK reaction: Still at target, but services remains sticky.

- por

- 17 Julio 2024 (3 min de lectura)

China reaction: Q2 GDP marks the start of The Third Plenum

- por

- 15 Julio 2024 (5 min de lectura)

US reaction: Services inflation makes pivotal shift lower

- por

- 11 Julio 2024 (5 min de lectura)

China reaction: CPI inflation moderates as PPI narrows its fall

- por

- 10 Julio 2024 (3 min de lectura)

US reaction: Labour market achieving balance

- por

- 05 Julio 2024 (7 min de lectura)

Disclaimer

Este documento tiene fines informativos y su contenido no constituye asesoramiento financiero sobre instrumentos financieros de conformidad con la MiFID (Directiva 2014/65 / UE), recomendación, oferta o solicitud para comprar o vender instrumentos financieros o participación en estrategias comerciales por AXA Investment Managers Paris, S.A. o sus filiales.

Las opiniones, estimaciones y previsiones aquí incluidas son el resultado de análisis subjetivos y pueden ser modificados sin previo aviso. No hay garantía de que los pronósticos se materialicen.

La información sobre terceros se proporciona únicamente con fines informativos. Los datos, análisis, previsiones y demás información contenida en este documento se proporcionan sobre la base de la información que conocemos en el momento de su elaboración. Aunque se han tomado todas las precauciones posibles, no se ofrece ninguna garantía (ni AXA Investment Managers Paris, S.A. asume ninguna responsabilidad) en cuanto a la precisión, la fiabilidad presente y futura o la integridad de la información contenida en este documento. La decisión de confiar en la información presentada aquí queda a discreción del destinatario. Antes de invertir, es una buena práctica ponerse en contacto con su asesor de confianza para identificar las soluciones más adecuadas a sus necesidades de inversión. La inversión en cualquier fondo gestionado o distribuido por AXA Investment Managers Paris, S.A. o sus empresas filiales se acepta únicamente si proviene de inversores que cumplan con los requisitos de conformidad con el folleto y documentación legal relacionada.

Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA Investment Managers Paris, S.A.

La información aquí contenida está dirigida únicamente a clientes profesionales tal como se establece en los artículos 194 y 196 de la Ley 6/2023, de 17 de marzo, de los Mercados de Valores y de los Servicios de Inversión.

Queda prohibida cualquier reproducción, total o parcial, de la información contenida en este documento.

Por AXA Investment Managers Paris, S.A., sociedad de derecho francés con domicilio social en Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, inscrita en el Registro Mercantil de Nanterre con el número 393 051 826. En otras jurisdicciones, el documento es publicado por sociedades filiales y/o sucursales de AXA Investment Managers Paris, S.A. en sus respectivos países.

Este documento ha sido distribuido por AXA Investment Managers Paris, S.A., Sucursal en España, inscrita en el registro de sucursales de sociedades gestoras del EEE de la CNMV con el número 38 y con domicilio en Paseo de la Castellana 93, Planta 6 - 28046 Madrid (Madrid).

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.