US reaction: Payrolls stay strong

- 05 Abril 2024 (5 min de lectura)

Payrolls for March once again defied expectations posting the third consecutive major upside surprise. Payrolls rose by 303k in March, once again exceeding the consensus (214k) and our own expectations. Exhibit 1 illustrates that March’s rise defied the only indicator that has been even close to tracking payrolls growth over the past 3 years. Unlike in previous month’s where a strong front month was offset by previous revisions, this time February’s initial estimate was only revised down 5k to 270k and January was revised higher by 27k. The 3-month trend increase was basically stable at 276k, but this was the firmest since June last year and an acceleration from the pace set at the end of last year. The acceleration this month came from jobs in the goods industry – manufacturing no longer shedding jobs and a 13k rise in construction jobs. Services job gains were unchanged overall at 190k.

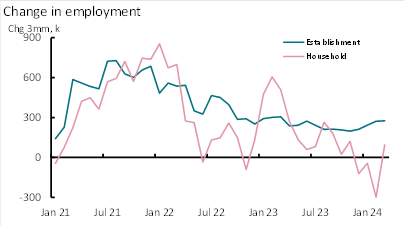

Not only was this month’s strong payrolls gain not tempered by prior revisions, it was also not mitigated by weakness in household employment. This measure rose by 498k in March, leaving the level just 84k lower over the past six months, with the 3-month trend increase moving back into positive territory (+94 vs -299 in February, Exhibit 2). This still leaves some trend divergence between the tow metrics, but it is not as stark as before. The sharp jump in employment was met with a much smaller dip in unemployment, which fell back to 3.8% - in line with expectations - reflecting another strong increase in labour supply – up 469k on the month or 0.28% - the strongest monthly gain since August. In turn this lifted the labour force participation rate back to 62.7%, closer to last summer’s post-pandemic high.

The in-line unemployment rate was matched by an in-line 0.3% monthly increase in March’s total average hourly earnings, which saw the annual rate decelerate to 4.1% and its lowest since mid-2021. The more recent trend 3-monthly annualized growth rate edged higher to 4.1% in March from 4.0% in February, nudged by modest upward revisions to the prior two month rates. The trend in non-supervisory earnings is somewhat weaker, slowing to 3.9% 3-month annualized in March = its weakest since October. We continue to argue that 4.1% is not far from the range of wage growth that the Fed would deem consistent with its inflation target, a range likely to be around 3.5-4.0%.

Today’s payrolls report is not the be all and end all for the Fed’s expected easing cycle. Indeed the Fed will see two more payrolls reports before June’s meeting – not to mention three inflation prints, starting with next week’s. The continued upside surprise in jobs growth continues to point to an economy still in good health – defying some of the more cautious Fed commentary if any reversals started to emerge. However, from an inflationary perspective, the fact that despite strong jobs growth unemployment has not moved much – still someway from its recent lows – and vacancy rates are still lower (the vacancy-unemployment rate is near a 3 year low) all suggest that the labour market does continue to “come into better balance” as the Fed described at its last meeting. Average earnings deceleration is a further testimony to that. However, the still solid state of the labour market would likely lead the Fed to consider it had more time to consider easing policy and we think a deceleration is likely to be necessary from here for the Fed to deliver a cut in June.

Given market doubts over Fed rate cuts, the reaction to today’s report was predictable, but not excessive. The chance of a June cut was reduced from 92% to just 58%. December went from 90% chance of 3 cuts to just 70%. Meanwhile 2-year and 10-year US Treasury yields rose 6bps to 4.71% and 4.38% respectively and the dollar rose by 0.4% against a basket of currencies. To our minds, markets correctly remain focused on a June cut, but with scant chance of the Fed moving before June and a real risk that it moves later, this risk skew should affect the chances priced for June now. We continue to expect a June move as we expect some deceleration of employment growth over the coming months and expect to see core measures of inflation resume softer growth over the coming months. However, the strength of employment growth, albeit mitigated by stronger labour supply growth has resulted in upside risks to our growth outlook for this year and reduces the chances of the Fed quickening its pace of cuts later this year to total four cuts.

Exhibit 1: Payrolls defy survey evidence

Source: BLS, NFIB, April 2024

Exhibit 2: Divergence in employment measures unwinds

Source: BLS, April 2024

Artículos relacionados

Ver todos los artículos

Pushing the Walls

- por Gilles Moëc

- 22 Julio 2024 (10 min de lectura)

Finanzas en 2 minutos: El BCE mantiene los tipos de interés sin cambios; El FMI aumenta su previsión de crecimiento mundial para 2025

- por

- 22 Julio 2024 (3 min de lectura)

ECB Review: No commitment, no guidelines, no…thing

- por François Cabau,

- 19 Julio 2024 (3 min de lectura)

UK reaction: Still at target, but services remains sticky.

- por

- 17 Julio 2024 (3 min de lectura)

China reaction: Q2 GDP marks the start of The Third Plenum

- por

- 15 Julio 2024 (5 min de lectura)

Changing of the Guards

- por Gilles Moëc

- 15 Julio 2024 (10 min de lectura)

Advertencia sobre riesgos

El valor de las inversiones y las rentas derivadas de ellas pueden disminuir o aumentar y es posible que los inversores no recuperen la cantidad invertida originalmente.